Stocks

DBS soars to all-time high. Still worth buying at 6.1% dividend yield?

By Beansprout • 02 May 2024 • 0 min read

DBS' share price reached an all-time high after its reported a record first quarter profit and raised its dividends. We find out if DBS is still worth considering for dividend investors.

In this article

What happened?

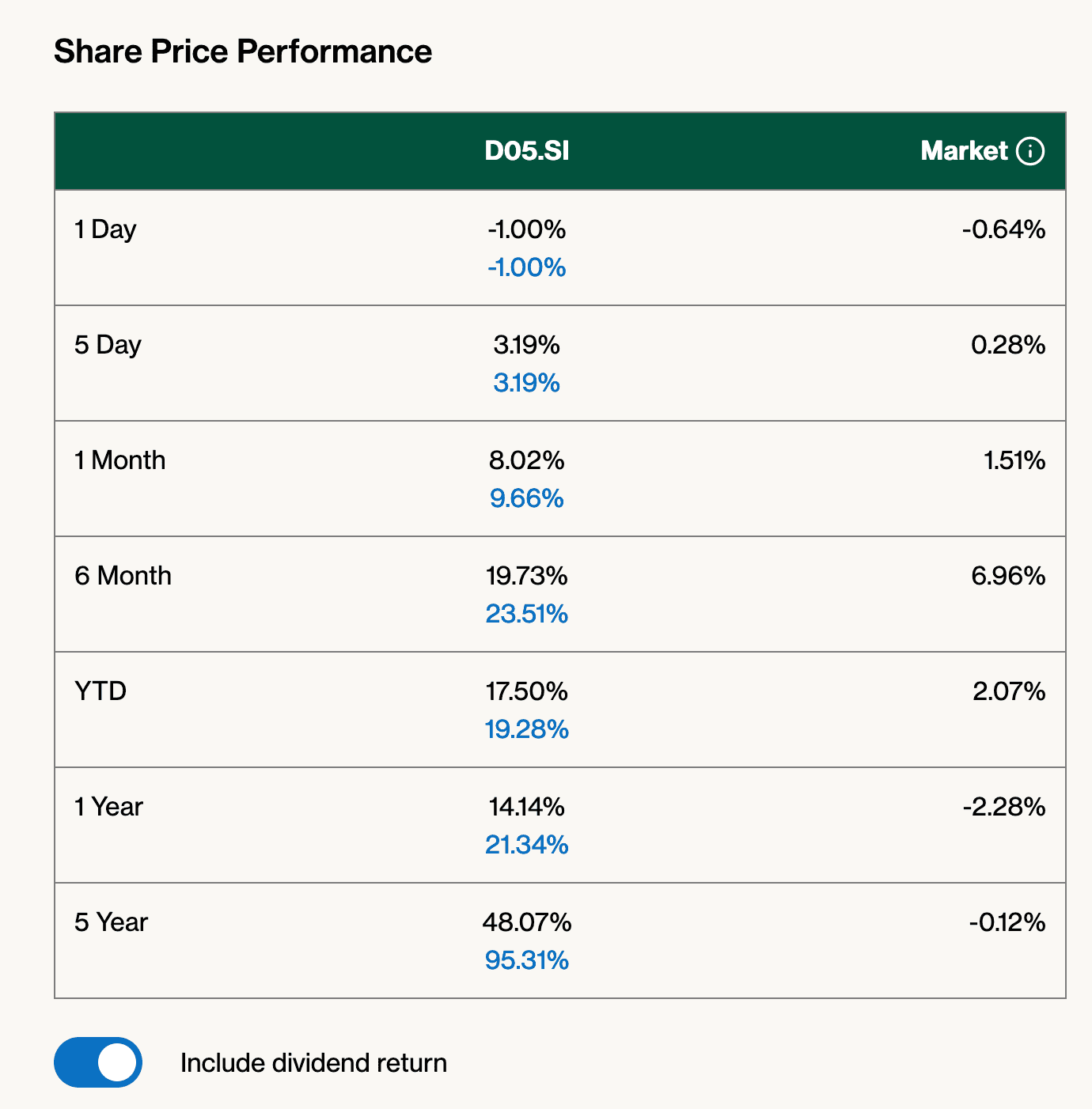

DBS’ share price has been scaling new heights.

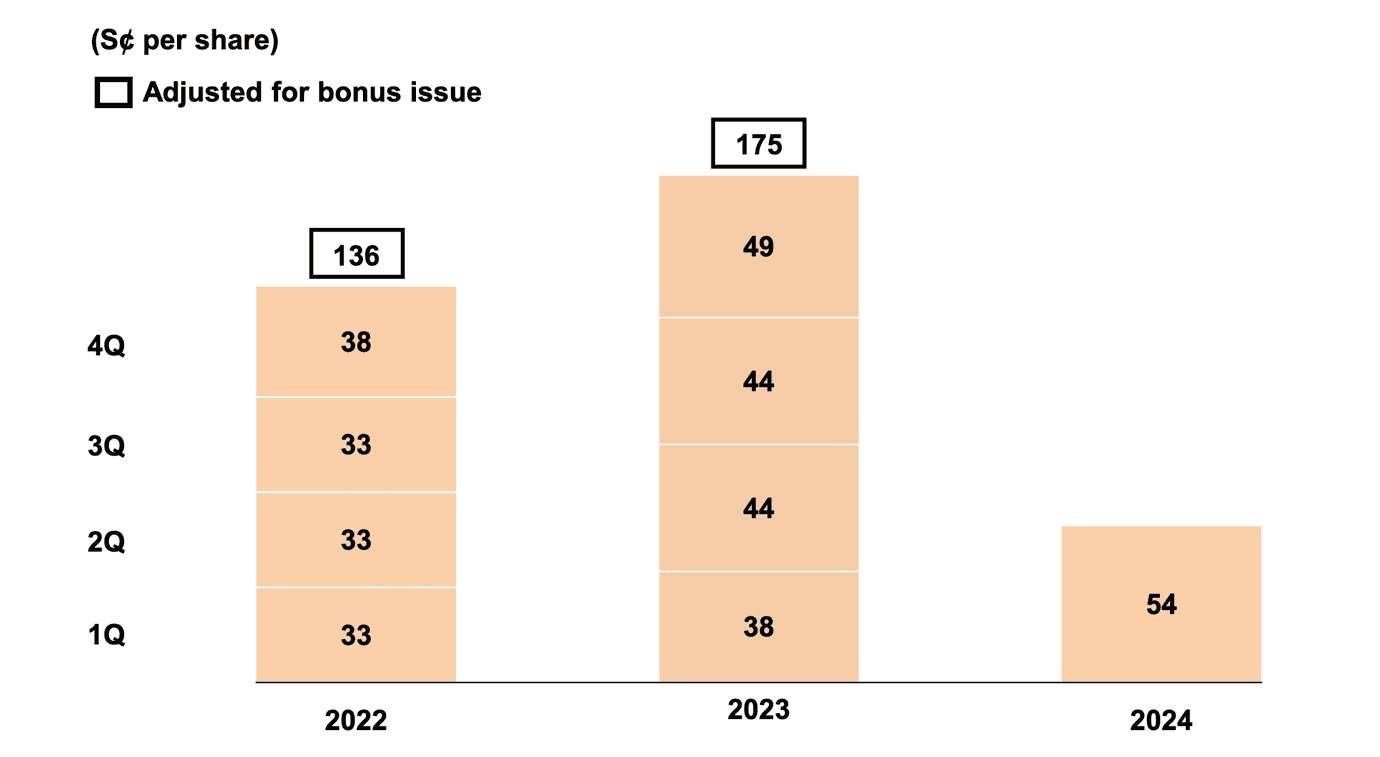

Its share price has climbed steadily to reach an all-time high of $36.00, after the company announced a record full year profit and an increase in dividends in 2023.

I must highlight that this share price of $36.00 is after adjusting for its recent bonus issue.

This would also make DBS the first Singapore-listed stock to exceed a market capitalisation of S$100 billion.

Looking at its performance year-to-date, DBS has gained close to 20%, far exceeding the Straits Times Index’s gain of 2%.

DBS has also performed better than UOB and OCBC so far this year.

More recently, DBS reported a record high first quarter net profit of $2.96 billion, an increase of 15% compared to the previous year. DBS also achieved another record high ROE of 19.4%.

With the higher profit, DBS increased its dividends per share to 54 cents in the first quarter of 2024 from 38 cents in the same period last year.

Since many investors in the Beansprout community appear fairly interested in DBS' stock, I shall dive deeper into DBS’ first quarter results to find out if there may be more upside after its stellar performance in recent months.

What you need to know about DBS’ record first quarter profit

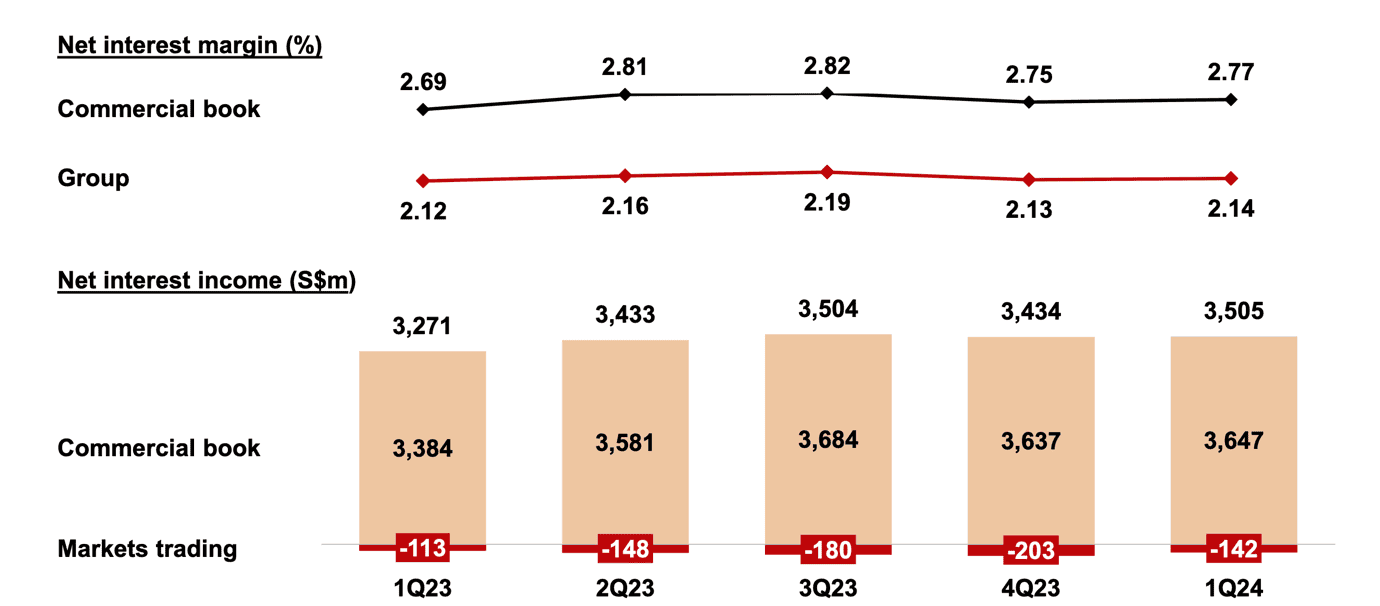

#1 - Net interest margin expanded

DBS’ net interest margin (NIM) expanded to 2.14% from 2.13% in the previous quarter, reversing the decline in the previous quarter.

This was driven by re-pricing of assets that were locked in at lower fixed rates previously.

Loans growth surprised with an increase of 2.1% compared to the previous quarter, led by 3% increase in non-trade corporate loans. However, the rate of growth might ease in 2Q as HK loans demand migrates to lower-cost China.

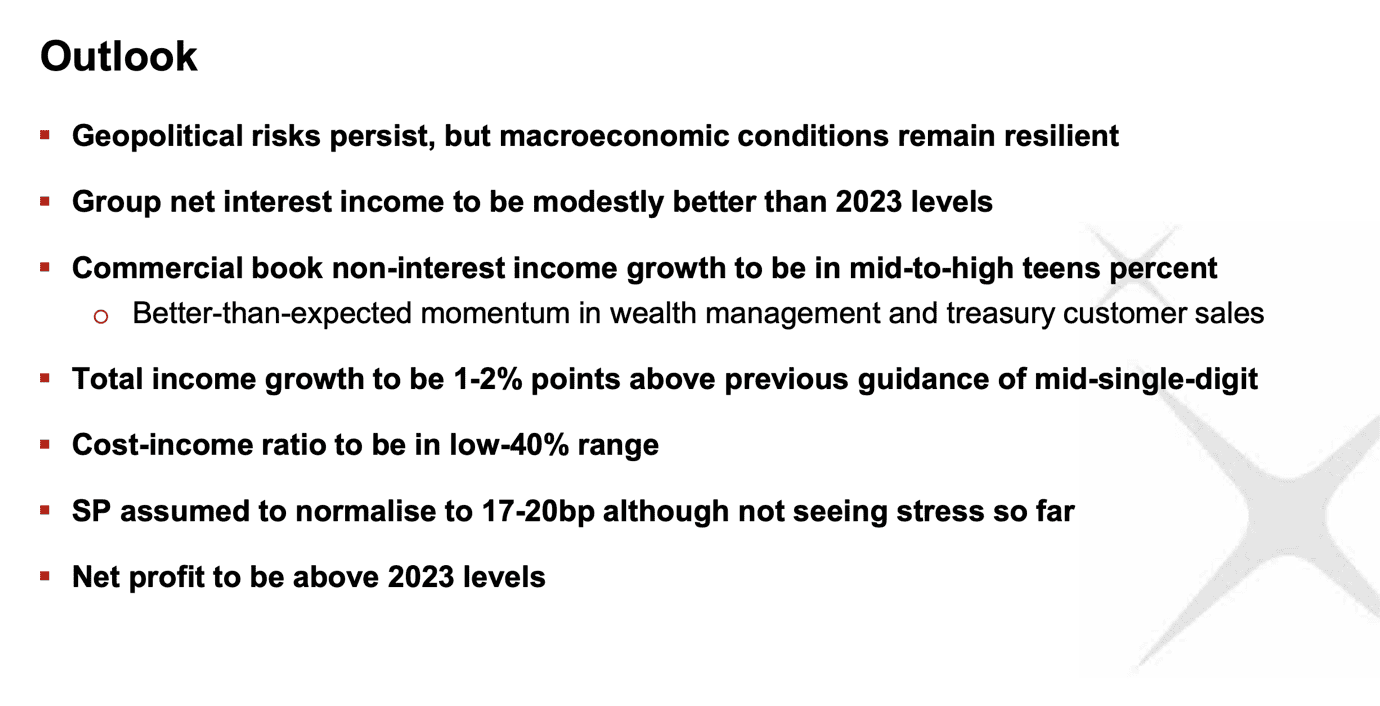

DBS maintained its guidance for flat to moderate decline in NIM in 2024 (from 2023 exit NIM of 2.13%), factoring in two rate cuts this year.

The expectation of a moderation in NIM in subsequent quarters is premised on two factors: 1) Management is focused on growing net interest income through longer duration assets; and 2) Deposit rates are likely to be held up by the higher-for-longer rates, giving less room to improve cost of funds.

Nevertheless, management also stated that NIM could be higher in FY24 if there is no rate cut.

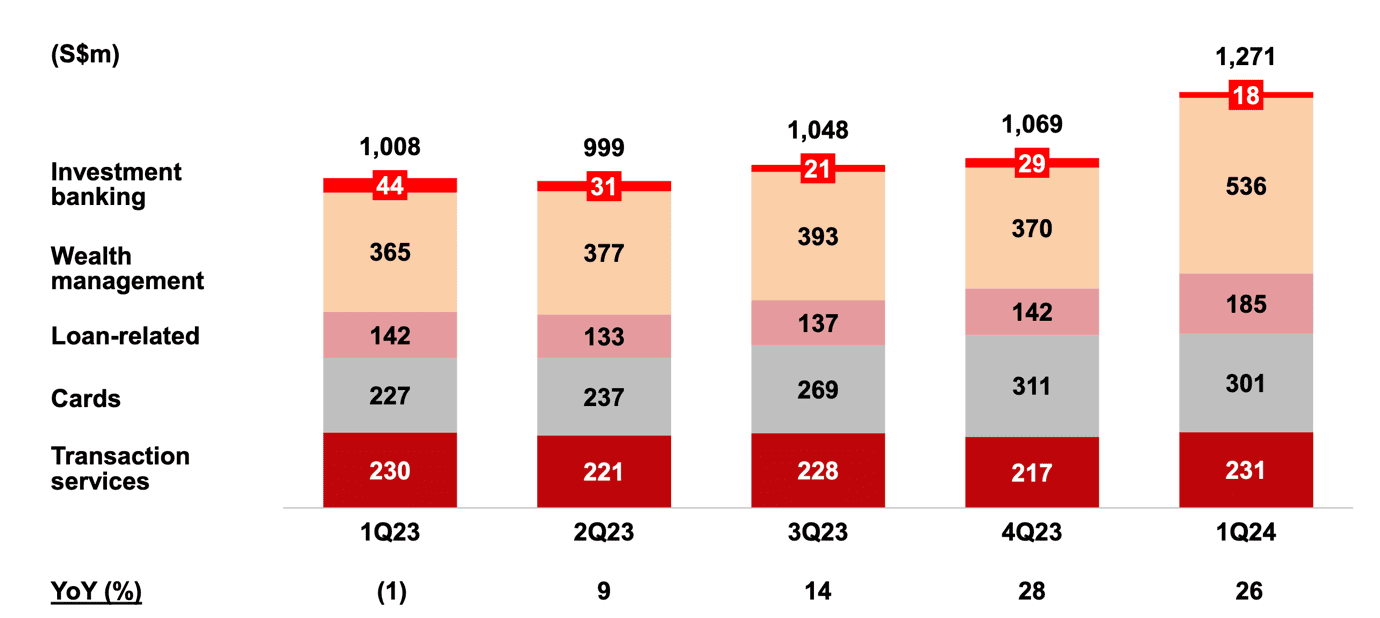

#2 - Fee income surprised positively

Non-interest income growth also surprised positively, and now accounted for 30% of total income (4Q23: 25%).

Total fee income increased to S$1.27 billion in the first quarter of 2024, an increase of 26% compared to the previous year.

A more buoyant equity market lifted AUM and the shift from deposits into investments, bolstering wealth management and loans-related fees.

Card fees was 32.6% higher year-on-year, partly due to the inclusion of Citi Taiwan from Aug 2023.

Investment banking was the only weak spot, with low M&A and capital market activities.

#3 - Asset quality remains good

Despite the firm interest rates, asset quality remains healthy. Specific provisions as a percentage of total loans were a low 10bp (4Q23: 11bp).

Still, DBS expects credit cost at 17-20bp for FY24, taking into account potential risks of persistent high rates on SME and consumer loans, though it has not seen any weakness yet.

NPL ratio stays low at 1.1% (4Q23: 1.1%).

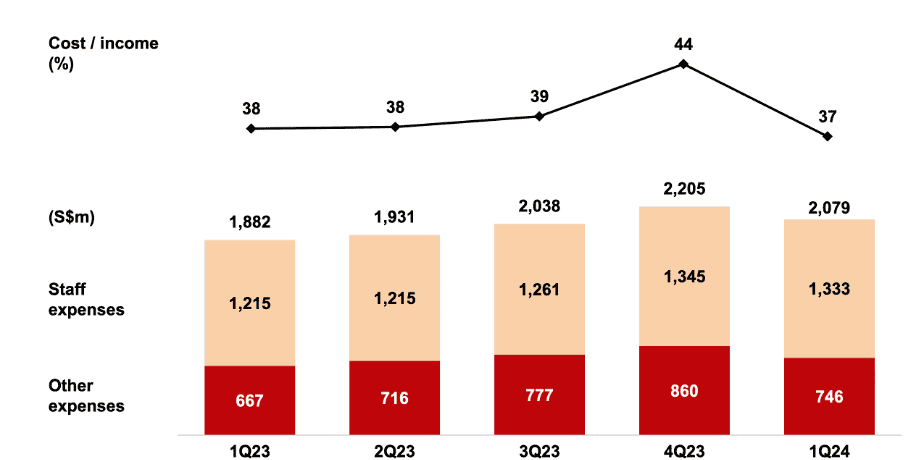

#4 - Cost to income ratio improved

Cost to income ratio (CIR) was lower at 37.4% (1Q23: 38.1%), as income growth outpaced costs increase.

Operating costs rose 10.5% yoy with Citi Taiwan accounted for 5.0%. Management however, expects CIR to be in low 40% range for FY24, with higher spending on technology.

#5 – Guidance raised

Management of DBS raised their guidance for profit in 2024. It now expects higher net profit for FY24, versus flat estimates previously.

This is driven by expectation of higher net interest income in FY24, versus stable guidance previously.

It also expects total income growth of 6-7% in FY24, higher than previous guidance of mid-single-digit.

What would Beansprout do?

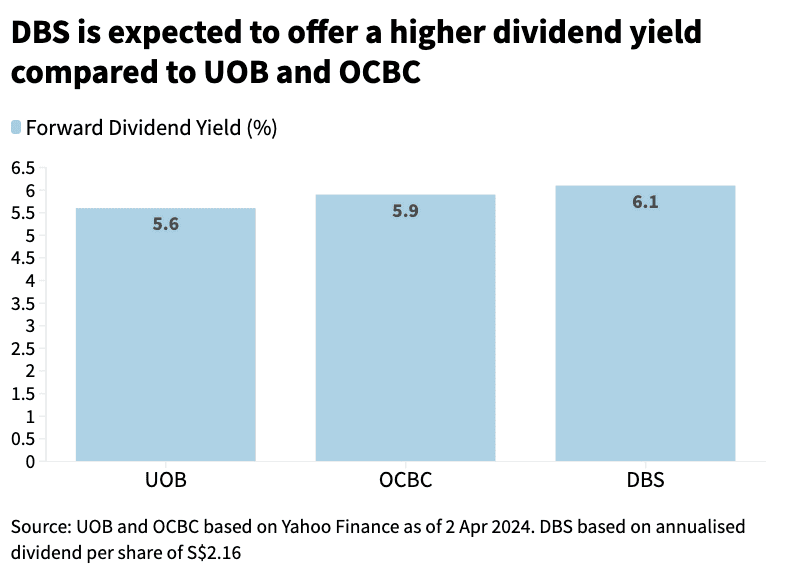

Despite DBS’ strong share price performance year-to-date, it continues to offer a dividend yield of 6.1% based on the expected dividend per share of S$2.16 for the full year.

This would be higher than the dividend yield on the Straits Times Index (STI).

Find out how much dividends you would have received as a shareholder of DBS in the past 12 months with the calculator below.

DBS’ dividend yield would also be higher than the expected dividend yield on UOB of 5.6%, and the expected dividend yield on OCBC of 5.9%.

On a macro level, the latest Fed’s statement points to less likelihood of rate cuts this year. A higher for longer rate environment is positive for net interest margin.

At the same time, wealth management remains the bright spot, and a key earnings growth driver. DBS received net new money of S$24b per year in 2022 and 2023, and a further S$6b in 1Q24. This should underpin growth for wealth management and related fee income.

Hence, we would continue to consider DBS as an income investor for the dividend yield that it offers.

The record date for DBS’ interim dividend of 54 cents will be on 10 May, and the dividend will be paid on or about 20 May 2024.

You can refer to our DBS stock page to get updates on the latest DBS dividend dates.

If you are interested to learn about income opportunities in the Singapore market, join our upcoming webinar on 14 May 2024 to find out how you can identify these opportunities.

Join the Beansprout Telegram group to get the latest insights on Singapore bonds, stocks, REITs, and ETFs.

Related links:

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments